Oklo Stock: What the Data Says vs. the Broader Tech Hype

The $20 Billion Question Haunting Oklo Stock

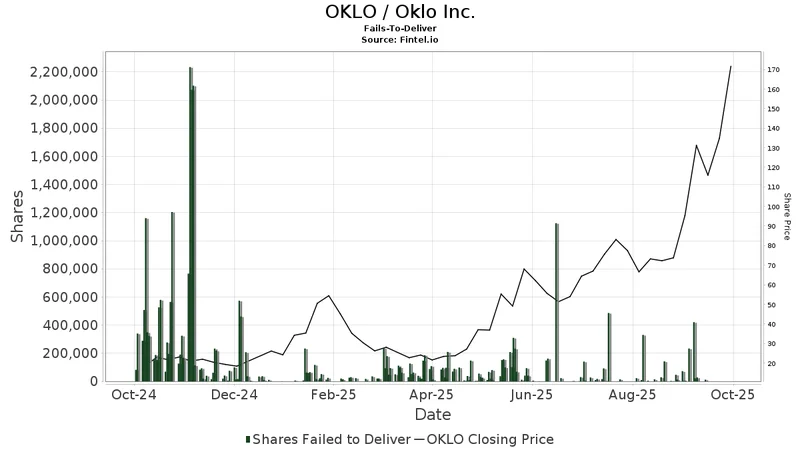

The chart for Oklo Inc. (OKLO) over the past few weeks looks less like a stock ticker and more like a seismograph reading during an earthquake. After an absolutely parabolic ascent—a run of between 300% and 400% year-to-date—the inevitable force of financial gravity has reasserted itself. The stock has pulled back sharply, shedding 20-30% of its value in a handful of trading sessions and is now nervously testing a prior breakout level for support. This pullback has put the stock on many investors' radars, prompting the central question in Leading Stocks Pullback: Should Investors Buy Now? (IREN, NBIS, OKLO).

For the momentum chasers who rode the wave up, this feels like a catastrophe. For those who watched from the sidelines, it feels like vindication. The chatter online, which I treat as a qualitative, anecdotal data set, shows a clear bifurcation: panicked calls to "buy the dip" on one side, and cynical "I told you so" declarations on the other.

But both camps are missing the point. The recent drop in the `oklo stock price` isn't the real story. It's merely a symptom of a much more fundamental and unsettling question. The real story is how a pre-revenue company, years away from generating any meaningful cash flow, managed to command a $20 billion market capitalization in the first place.

This isn't a critique of Oklo's mission. The company is working on advanced compact nuclear reactors, a field that is undeniably critical for the future of energy. The technology is fascinating, and its success would be a net positive for the world. But my job isn't to evaluate engineering roadmaps; it's to evaluate financial instruments. And as a financial instrument, OKLO at $20 billion was a masterpiece of narrative over numbers. It’s like a skyscraper with a beautiful, 100-story facade built on a foundation poured for a two-story office building. The recent sell-off isn't a demolition; it's just the first set of stress fractures appearing in the marble.

The Anatomy of a Narrative Bubble

Let’s be precise about the numbers. The stock didn’t just rally; it went vertical. We’ve seen similar moves in other narrative-driven stocks, from `tesla stock` (TSLA) in its early days to the more recent mania around `nvidia stock` (NVDA). The difference, however, is that during their most explosive growth phases, both Tesla and NVIDIA were posting staggering revenue and earnings figures. They were monetizing the hype. Oklo is not. It remains a speculative bet on future technology, which makes its valuation purely a function of belief.

Analyst Ethan Feller recently suggested that the stock may be in for a prolonged consolidation, similar to what was observed in AppLovin (APP) earlier this year. I find this comparison apt. My analysis suggests that after a stock experiences a 4x or 5x move in less than a year, the subsequent correction is rarely a quick V-shaped recovery. Instead, the stock enters a long, frustrating sideways channel as the early buyers take profits and the latecomers are slowly worn down. The stock corrected over 20%—to be more exact, 28.6% from its absolute peak at the time of this writing. This isn’t a dip; it’s a fundamental break in market structure.

Patience, as Feller notes, is the correct strategy here. But what are investors actually waiting for? Are they waiting for the chart to look better, or are they waiting for the company’s fundamentals to catch up to its astronomical valuation? If it’s the latter, they could be waiting a very, very long time.

And this is the part of the analysis that I find genuinely puzzling. The market has priced Oklo as if its success is not only probable but imminent and world-dominating. At a $20 billion valuation (a figure that places it among established, profitable enterprises), what possible upside is left? The current price seems to have factored in a decade of flawless execution, regulatory approval, and widespread adoption. It leaves absolutely no margin for the inevitable delays, cost overruns, and competitive pressures that every single hard-tech company in history has faced. The question isn't whether you should buy the dip. The question is, what future are you even buying at this price?

Price vs. Value: A Necessary Collision

The core of the issue is a methodological one. How do you value a company with no revenue, no product on the market, and a multi-year timeline to potential cash flow? The honest answer is that you can’t, at least not with any traditional framework. Any discounted cash flow model would be pure fantasy. Price-to-sales is infinite. You are left with one metric: sentiment.

The market for `smr stock` (Small Modular Reactors) and other next-gen tech like that of `ionq stock` (IONQ) has become a proxy for general market risk appetite. When investors feel bold, money pours into these stories. When fear creeps in, it evaporates just as quickly. OKLO became the poster child for this phenomenon. Its value wasn't tied to its own milestones, but to the market's willingness to dream.

This recent pullback represents the market's first moment of lucidity—the first time it has woken up and asked for something more than a good story. The retest of the breakout zone is technically significant, of course. A hold there could signal the start of a new base-building phase. A failure could see the stock give back another substantial portion of its gains.

But focusing on the daily chart action is like analyzing the brushstrokes on one square inch of a painting while ignoring the entire canvas. The bigger picture for Oklo has nothing to do with support levels or resistance lines. It has everything to do with the slow, grinding collision between an explosive stock price and a non-existent business value. For now, the price has won. History suggests that, eventually, value always does.

A Valuation in Search of a Business

Ultimately, the analysis of Oklo stock is simple. The recent 30% correction isn't a sign of failure or a fleeting buying opportunity. It is a necessary and healthy dose of reality. The stock isn't being punished; it's being repriced from a level of pure fantasy to something slightly less so. The fundamental discrepancy remains: a multi-billion dollar valuation for a company that, from a financial perspective, barely exists yet. Until Oklo can show a clear, tangible path to revenue—not just a compelling slide deck—its stock will remain an instrument of pure speculation, driven by market sentiment, not corporate performance. And sentiment, as we’ve just been reminded, is a notoriously fickle foundation on which to build a $20 billion company.

Tags: oklo stock

The Fight for NASA's Future: What's at Stake and Why It Matters More Than Ever

Next PostQBTS Warrant Redemption: A Price Analysis vs. Quantum & AI Stocks

Related Articles