Current Mortgage Rates: What You Need to Know Now

Beyond Fixed Horizons: Why Dynamic Finance, Not Just Tech, Is Your Future Superpower

Alright, let's talk about the future. Not just the shiny gadgets or the AI breakthroughs that grab all the headlines, but the underlying mechanisms that empower us to build that future. Because, frankly, if we're not thinking dynamically about everything, including our personal finances, we're already falling behind. I’ve spent years at MIT, diving deep into complex adaptive systems, and what I’m seeing in the seemingly mundane world of mortgage rates right now is a perfect microcosm of this truth.

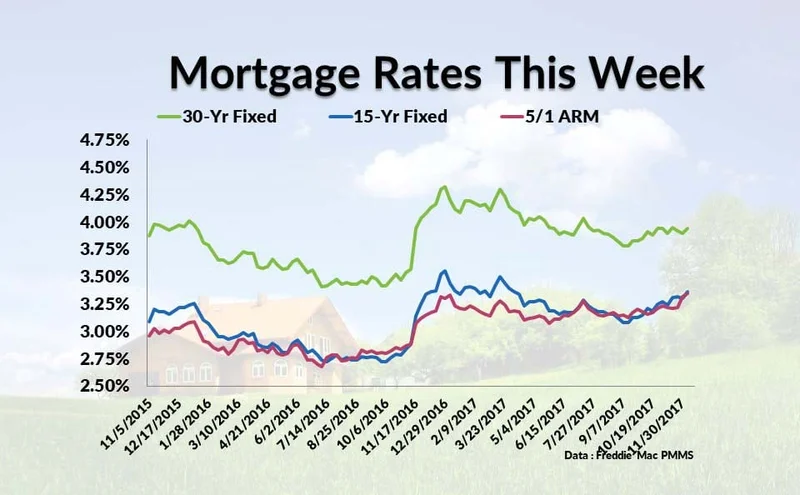

Most people, when they hear "mortgage," immediately picture that rock-solid fixed rate, right? It’s the comfort food of homeownership, the financial equivalent of a trusty old mainframe – predictable, reliable, but sometimes… a little rigid for the lightning-fast pace of modern life. And hey, I get it. A whopping 92% of folks choose fixed rates, and there’s absolutely nothing wrong with that certainty. But what about the other 8%? The innovators? The ones who understand that sometimes, the most powerful move isn’t to stay static, but to adapt, to pivot, to leverage the inherent dynamism of the market? That’s where adjustable-rate mortgages, or ARMs, come into play, and frankly, they’re a fascinating case study in strategic flexibility.

The Dance of Dynamic Decisions: Why "Fixed" Isn't Always "Forward"

Imagine for a second that you’re not just buying a house, you’re investing in a launchpad for your next big idea, or perhaps a temporary base camp before your next adventure. Our lives aren’t linear anymore. We're not all settling down in one place for 30 years with a gold watch at the end. We're digital nomads, serial entrepreneurs, global citizens. And for these dynamic lives, a static financial instrument can feel like trying to navigate a bustling city with a paper map from 1995.

This is where ARMs, particularly something like a 7/6 ARM – fixed for seven years, then adjusting every six months – become incredibly compelling. You get a lower introductory rate, a significant head start, before the market’s true ebb and flow influences your payments. It's like having a high-performance, fuel-efficient engine for the first seven years of your journey, giving you the power to accelerate your wealth building, invest in that side hustle, or simply save more aggressively. The financial data from top lenders like Bank of America, U.S. Bank, and Zillow Home Loans, showing rates from 5.500% to 6.250% for 7/6 ARMs, compared to what we know fixed rates often sit at, isn't just a number; it's an invitation to strategize. For up-to-date figures, consult the Current ARM mortgage rates report for Nov. 21, 2025. It's a clear signal that for those with a calculated plan, there's an opportunity here.

But let's be real, the idea of a fluctuating rate can feel like trying to catch smoke, can't it? This is where I believe the real breakthrough lies, not just in the ARM itself, but in how we approach it. It’s about leveraging foresight and understanding the underlying algorithms, the benchmark indices like SOFR, and the lender’s margins. In essence, you’re not just taking a loan; you’re engaging with a finely tuned financial algorithm. The speed of this is just staggering—it means the gap between today and tomorrow’s financial landscape is closing faster than we can even comprehend, and we need tools that can keep pace, not just passively react.

When I first started diving into how these rates are calculated, tied to something as fluid as the Secured Overnight Financing Rate, I honestly just sat back in my chair, speechless. It’s a beautiful, complex system, mirroring the very adaptive algorithms we build in tech. What this means for us is that financial literacy isn’t just about balancing a checkbook anymore; it’s about understanding the mechanics of dynamic systems. For those planning to flip a property, or investors who can adjust rents, or even first-time homebuyers facing elevated fixed rates today, an ARM isn't a gamble; it's a strategically deployed tool. It’s like opting for a modular, upgradeable operating system rather than a monolithic, unchangeable one.

The Ethical Algorithm: Balancing Opportunity with Responsibility

Of course, with great power comes great responsibility, right? This isn't a "set it and forget it" kind of deal. The flexibility of an ARM demands a proactive mindset. You’ve got to weigh your personal tolerance for uncertainty, your potential for relocation, and your long-term financial goals. What happens if your grand plan to flip that property hits a snag? Or if that "starter home" becomes your forever home because, let's face it, upgrading is tough for so many Millennials and Gen Z homeowners right now? It’s a critical moment of ethical consideration: are we truly preparing ourselves, and those we advise, for the dynamic shifts these instruments represent? Are we building the necessary personal financial resilience?

This brings me to a thought that often echoes in the Reddit threads I follow. I saw a comment recently, someone saying, "ARMs are just for high rollers or fools, way too risky." And I get that initial apprehension. It’s the human brain defaulting to safety, to the known. But here’s the reframe: What if ARMs, when understood and strategically utilized, are actually a tool for empowerment? What if they're not about chasing risk, but about optimizing opportunity in a world that refuses to stand still? It's like the early days of the internet; people thought it was just for academics or hackers, but it became the fabric of our lives. Dynamic finance isn't just for the niche; it's a skill set for the future.

We need to ask ourselves: are we truly leveraging every tool in our arsenal to navigate this rapidly evolving economic landscape? What kind of financial resilience are we building for ourselves and for future generations? The answers aren't simple, but they start with embracing the dynamic, not shying away from it.

The Future Isn't Fixed; Your Strategy Shouldn't Be Either.

We're living in an era defined by change, by innovation, by the constant hum of algorithms shaping our world. To ignore the dynamic possibilities in our financial lives is to ignore a fundamental truth of the 21st century. ARMs aren't just a niche product; they're a lesson in adaptive strategy, a blueprint for leveraging flexibility, and a powerful reminder that sometimes, the smartest move isn't to stay put, but to embrace the beautiful, complex dance of tomorrow.

Tags: current mortgage rates

SpaceX Launch: What's Next and the Starship Buzz

Next PostMSTR Stock: Bitcoin's Grip & Today's Price

Related Articles